| PREVIOUS | HOME | NEXT |

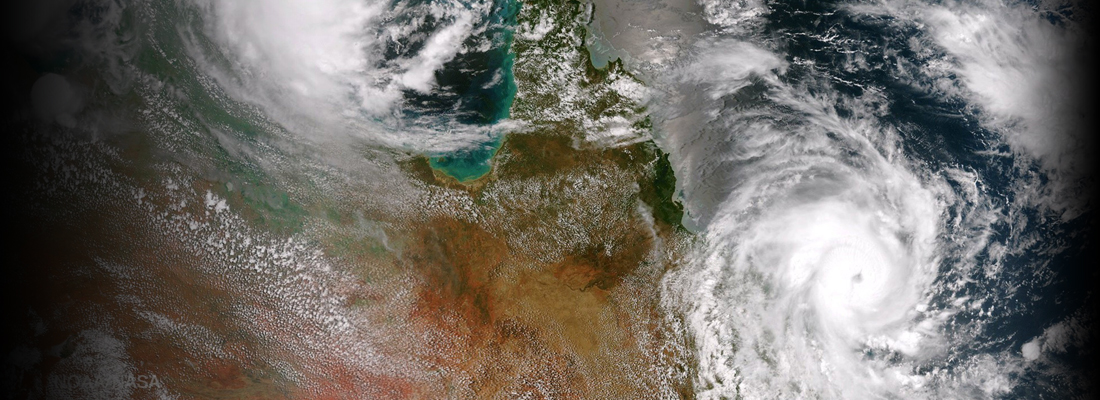

NIBA seeks clarification on clarification By Kate Tilley, Editor, Resolve The Federal Government’s decision to allow unauthorised foreign insurers (UFIs) to write north Queensland cyclone-prone risks will not result in “crazy prices”, says NIBA CEO Dallas Booth. He told an AILA Qld breakfast in Brisbane he considered UFIs would not be dealing direct with insureds, and brokers would remain intermediaries in the process. Finance minister Senator Mathias Cormann announced on October 23, 2014, that the Federal Government would “boost competition by clarifying that licensed brokers can sell policies from foreign insurers if they offer consumers a better price”. Mr Booth said much depended on what the government meant by “clarify” and he expected to see draft regulations soon. Brokers can place business with UFIs if the risk meets one of three specified criteria: Mr Booth said the onus was on brokers to be satisfied they could get a better deal with a UFI. The broker must do a proper investigation and keep written records of inquiries made and reasons for placing business with a UFI. He said the latest APRA statistics for 2013-14 showed $15.5 billion of insurance business was placed with APRA-regulated insurers; $1.8 billion with Lloyd’s, which is also APRA-regulated; and $1.3 billion with UFIs. In the six months to June 2014, 43% of the business placed with UFIs went to Singapore; 17% to the United Kingdom; and 5% to Bermuda. The breakdown by class was 71% fire/ISR; 3% professional indemnity; and 3% marine and aviation. Mr Booth said the “bulk” of UFI business was placed under the custom insured exemption, but not on the basis of price. Brokers cited Australian insurers’ inability to write the risk or “other circumstances”. The next steps were to determine what the Federal Government meant by “clarifying” brokers’ roles; clarifying what “substantially less favourable” actually meant; and determining what “reasonable inquiries” meant. “What records are to be kept? I suspect many brokers find it quite onerous.” Mr Booth said he did not expect any “wholesale intervention by UFIs, especially in personal lines”. He said actuarial group Finity Consulting had been contracted by ASIC to develop content for a website that compared prices on home & contents policies for the north Qld market. (Mr Booth was uncertain whether strata pricing was included, but Resolve can confirm it is not.) “My understanding is it’s an information site and will not sell policies. I’m not sure it will have a price engine behind it, just indicative prices, so people still need to talk to an insurer or a broker,” Mr Booth said. Another initiative the government had promised – engineering assessments for north Qld strata buildings – was in progress. He said the Insurance Council of Australia was working with James Cook University and there was “a lot of emphasis on the risk itself” and assessing each risk individually. The Government Actuary had released two reports on north Qld claims and premium pricing and confirmed that insuring north Qld properties was more expensive than other locations because of the cyclone risk. “It’s that simple.” Mr Booth said the reports also confirmed insurers had not charged the right price for the risk for a decade and “a dramatic increase hurts”. “The north Qld market is still very difficult because it’s high risk. We must find other ways to make the risk more affordable and insurance sustainable,” he said. About two years ago, with only one or two insurers in the market, it was “almost total market failure”. A “substantial” part of Cairns was underinsured and it was a massive drain across the community when a cyclone occurred. Mr Booth expected the Federal Government to release draft regulations for consultation and to launch the comparator website and the engineering assessment program soon. The government was “aware of concerns” about UFIs and the importance of the “checks and balances” within Australia’s regulatory regime. The government “won’t do anything silly”, he said. And he was confident brokers would place business only with UFIs with solid security and claims-paying abilities. Mr Booth said governments controlled the built environment and there were “a lot of insane things happening” with houses and nursing homes being built on flood plains and in creek beds. Although there was evidence more stringent building standards were “doing their job”. Cairns broker John Devaney, from Joe Vella Insurance Brokers, agreed the “numbers are terrible” in north Qld, but asked for “some breathing space”. He suggested there were lessons from New Zealand’s Christchurch earthquakes, despite some mistakes having been made. “I’m not convinced of the mantra that [every region] should be profitable. It doesn’t work.” Mr Booth said insurers needed to satisfy APRA and shareholders and accurately price risks or risk “another HIH”. He agreed some retirees in north Qld could not pay body corporate fees because of high insurance premiums – “it’s a massive social issue”. Insurers “don’t want community-rated risk pools and there’s ample evidence, especially in the US, of them failing. The government then finds itself an insurer of first resort not last resort and with a lot of unfunded liabilities”. Mr Booth said the Australian Reinsurance Pool Corporation (ARPC), established to fund terrorism events, was the government’s response to a market failure and he acknowledged north Qld needed something “beyond the normal market process”. He urged the Federal Government not to discount a pool arrangement before carefully analysing the prospect. “We need a smoothing mechanism and models are available that could work.” When disaster occurred “someone must pay – either policyholders through premiums or the community through taxes or a smoothing mechanism that spreads the cost”, Mr Booth said. |

Resolve is the official publication of the Australian Insurance Law Association and

the New Zealand Insurance Law Association.