| PREVIOUS | HOME | NEXT |

Conformity clause enables claim denial

by Resolve Editor Kate Tilley

Insurers seeking to rely on exclusion clauses that refer to the outdated Quarantine Act 1908 to avoid Covid-19-related claims, will hope their policies include conformity clauses.

Lloyd’s syndicates have successfully argued that a conformity clause within a policy enables then to deny indemnity, despite the policy listing the former Act, which had been replaced before the policy’s inception.

Federal Court Justice Jayne Jagot on 10 March 2022 found the words “or other diseases declared to be quarantinable diseases under the Australian Quarantine Act 1908”, which appeared in clause 7 of a policy written by Certain Underwriters at Lloyd’s of London for Dural 24/7 Pty Ltd, ought to be read as “or other listed human diseases under the Biosecurity Act 2015 (Cth)”.

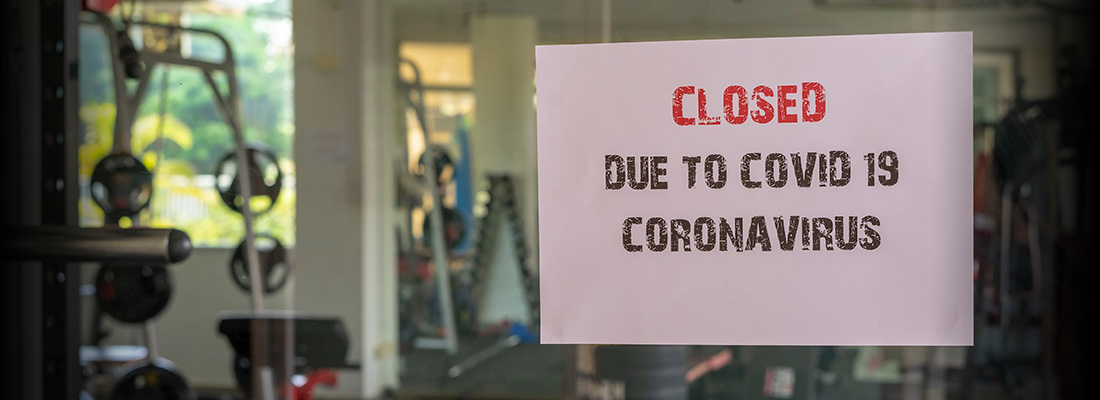

Dural 24/7 operated a Snap Fitness gym franchise at Dural NSW and the policy was in force from 1 January 2020 to 1 January 2021.

Human disease

On 16 June 2016, the Quarantine Act was replaced by the Biosecurity Act, which makes no reference to “quarantinable disease”. Covid-19 was listed as a human disease within the meaning of the Biosecurity Act on 21 January 2020.

In December 2020, Dural 24/7 lodged a claim via its broker seeking indemnity for Covid-19-related business interruption losses. The insurers denied indemnity.

A section of the policy headed “Information”, had a sub-heading “Conformity”, which included, among other things, the words: “References to a statute law also include all its amendments or replacements.”

Clause 7 of the policy, called ‘extension of cover’ indicated it did not apply in cases of “diseases declared to be quarantinable diseases under the Australian Quarantine Act 1908”.

The insurers argued the conformity clause operated for “all” amendments and replacements of any statute. They said the word “all” did not permit any reading down of the conformity clause’s reach. If a new statute law replaced a previous statute law, the conformity clause meant any reference to a previous statute was to be read as including a reference to a new statute.

They cited the explanatory memorandum for the Biosecurity Act, which noted it replaced the Quarantine Act.

Fundamentally different

The insured’s lawyers argued the Biosecurity Act was not a “replacement” of the Quarantine Act within the meaning of the conformity clause, and the concept of listing human diseases did not replace the concept of declaring quarantinable diseases.

They argued the new law was “fundamentally different”, not a replacement, and that the conformity clause applied only to prospective replacements to statute laws, not replacements that had already occurred before policy inception.

The insured argued a “statute” and a “statute law” were not the same thing. They also argued that if “replacement” did not mean “equivalent”, but was extended to include fundamentally different statute laws, there would be no certainty of contract.

Justice Jagot said: “There is no commercial or logical reason to infer that, in referring to ‘a statute law’, the parties commonly intended to mean anything more than a ‘law’ the source of which is a statute.”

She said the distinction the insured sought to draw between a statute and a provision of a statute, in the context of the conformity clause, was unsound.

Broad meaning

“A ‘statute law’ may encompass a statute as a whole or a specific provision of a statute. The relevant issue is whether the ‘statute law’ under consideration … has been amended or replaced.”

She rejected the insured’s attempt to distinguish different types of laws, saying: “Provided there is a ‘law’ (a legally enforceable or recognised right, duty, status or relationship) and the source of that law is a statute, then that law is ‘a statute law’.”

She decided the parties’ intent was to adopt a broader meaning for “replacement” (ie, “this for that”) rather than a narrow (“like for like”) interpretation.

“The high degree of certainty which the parties to a policy of insurance may be taken to have desired is better served by the ordinary broad meaning of ‘replacement’. This means, as the conformity clause expressly states, ‘all’ replacements of ‘a statute law’ are included within the scope of the clause.”

Justice Jagot said the subject matter of both Acts was substantially the same – the identification of human diseases to enable public officials to take steps to control and eradicate the disease.

Policy inception

She also rejected an argument the conformity clause intended only to reference a statute law in force at the time of inception of the policy.

Justice Jagot said an ordinary reader would “understand the reference to be to any statute law mentioned in the policy, whether or not it remained in force or in the form identified in the policy. … the focus of the relevant sentence in the conformity clause is not the statute law itself, but the reference to the statute law in the policy”.

She said there was no justification for restricting the conformity clause to amendments or replacements that came into effect after the policy’s inception.

“It would not be assumed or inferred that parties to the policy were scrutinising all amendments and replacements to statute law mentioned in the policy to ensure all such references were up to date as at inception of the policy.

“One purpose of the relevant sentence in the conformity clause is to ensure the parties did not have to do so. Another purpose is to ensure the references remain current throughout the life of the policy,” she said.

Certain Underwriters at Lloyd's of London v Dural 24/7 Pty Ltd [2022] FCA 206 (10 March 2022)

Read Marsh’s commentary on the Dural case and other Covid-19-related business interruption cases.

Resolve is the official publication of the Australian Insurance Law Association and

the New Zealand Insurance Law Association.